Sreeram Viswanath

Expert

Published on: Mar 28, 2026

GST Input Tax Credit

GST Input Tax Credit mechanism helps in avoiding double taxation and the cascading effect of taxes. The purpose of this article is to explore its applicability in the various facets of the Goods and Services Tax.

Pre-Requisites to Claim Input Tax Credit

A registered person must fulfil the following criteria to claim input tax credit:

- The registered person must possess a copy of the GST invoice, or debit note which was issued by the supplier, or some other documents as prescribed.

- The goods or services received by the registered person should tally with the Input Tax Credit availed by the applicant.

- The tax charged with respect to such supplies has been actually paid to the Government, either in cash or through the utilization of Input Tax Credit admissible in respect of the supply made.

- The registered person should have filed the GST returns.

GST Registration Required to Claim Input Tax Credit

GST Input Tax Credit can be claimed only be persons having

GST registration. However, those obtaining GST registration for the first time can claim input tax credit as follows:- A person applying for new registration within 30 days of becoming liable for registration can claim Input Tax Credit for taxes paid for inputs held in stock, as well as inputs contained in semi-finished or finished goods held in stock as on the date when he/she became liable to be taxed.

- A person applying voluntarily for new registration can claim Input Tax Credit on inputs held in stock and inputs contained in semi-finished or finished goods held in stock as on the date of grant of registration.

The below-mentioned criterion doesn't come under the purview of Input Tax Credit, with regards to registration of persons:

- Capital goods held by a person as on the date of registration will be exclusive of Input Tax Credit.

- Input Tax Credit can't be claimed for the person who has applied for registration beyond the prescribed period of thirty days, with respect of goods held in stocks and inputs contained in semi-finished or finished goods held in stock as on the date in which he becomes liable for registration.

Section 18 of CGST Act

As already seen, Section 18(1) of CGST Act entitles a registered person to claim input tax credit by filing a declaration in Form GST ITC 01. The following mentions the timeline for claiming credits for inputs in stock in finished, semi-finished or capital goods:

- If claimed only once by a taxpayer during his/her lifetime - the date prior to the date of registration.

- If claimed during the financial year – the day prior to the supposed date of payment of tax under section 9.

- Claims, as per clause (d) of sub-section (1) of section 18 – supplies undertaken by a registered taxpayer prior to the day of tax liability.

Goods Qualifying for the Provision

The taxpayer can claim the Input Tax Credit for the following goods:

- In-stock inputs.

- Semi-finished or finished stock of inputs.

- Capital goods (if a composition dealer withdraws from a composition scheme or where converting exempted goods into taxable ones).

Conditions for the Claim

The following taxpayers are included under the purview of Input Tax Credit (ITC):

- Taxpayers granted with GST registration within the timeframe of being liable to GST provisions, barring those under voluntary registration.

- Taxpayers with the details on purchases on or after the appointed day but prior to the registration, barring those covered under composition scheme or voluntary registration scheme.

Declaration of Claims on GST Portal

Since the basics are now done with the fundamentals, let us dive into the application procedure through which the claim of ITC can be filed and declared:

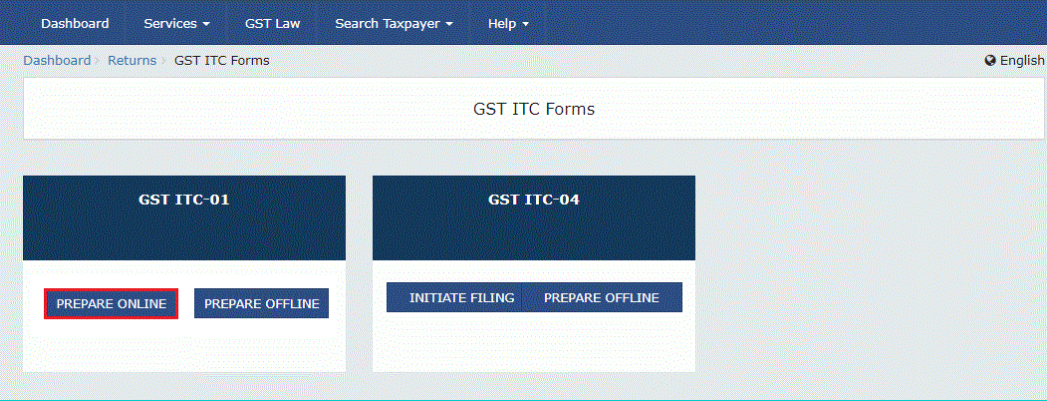

Step 1: Login The taxpayer may initiate the proceedings by login into the official GST portal. Step 2: Login The user can log in to the portal using his/her credentials. Step 3: ITC Forms The user may now choose the option of ‘Returns’ and ‘ITC Forms’ from the Services drop-down menu. ITC Forms

Step 4: Actions in the Form Page

The GST ITC Form page is displayed. The user may select the ‘Prepare Online’ option to prepare the statement by furnishing the requisite entries on the GST portal.

ITC Forms

Step 4: Actions in the Form Page

The GST ITC Form page is displayed. The user may select the ‘Prepare Online’ option to prepare the statement by furnishing the requisite entries on the GST portal.

Prepare Online

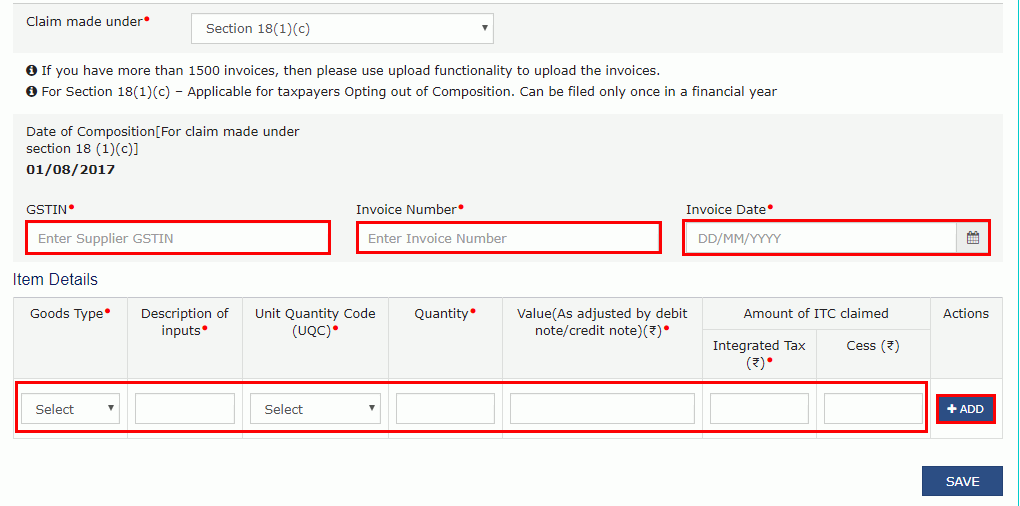

Step 5: Declaration for Claim

The appropriate selection may be selected from the claim made under the drop-down list.

Step 6: Furnish Details

In the following page, the requisite details must be specified, which includes:

Prepare Online

Step 5: Declaration for Claim

The appropriate selection may be selected from the claim made under the drop-down list.

Step 6: Furnish Details

In the following page, the requisite details must be specified, which includes:

- The GSTIN of the supplier.

- Invoice number.

- The date of invoice.

- Type of goods (to be selected among the options in the drop-down list).

- Description of inputs.

- Unit Quantity Code (again, to be chosen).

- The quantity of input.

- Invoice value.

- Amount of ITC claimed in the form of Central Tax, State/UT Tax, Integrated Tax, and Cess.

Add and Save

Add and Save

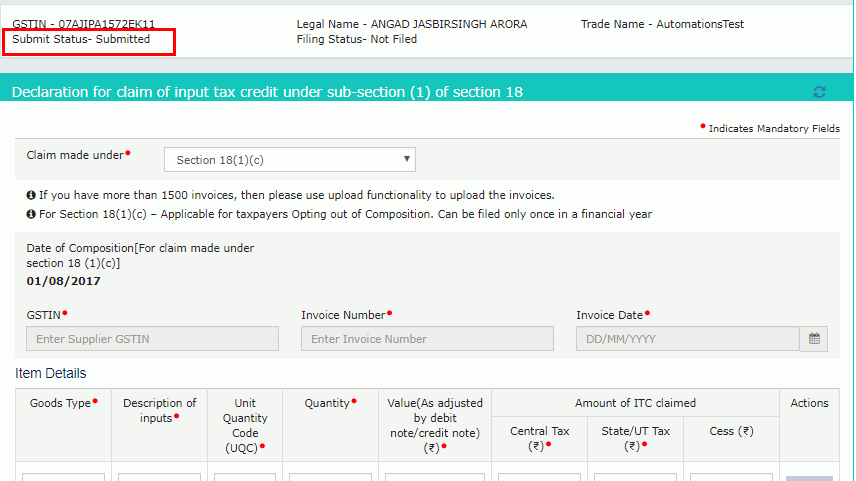

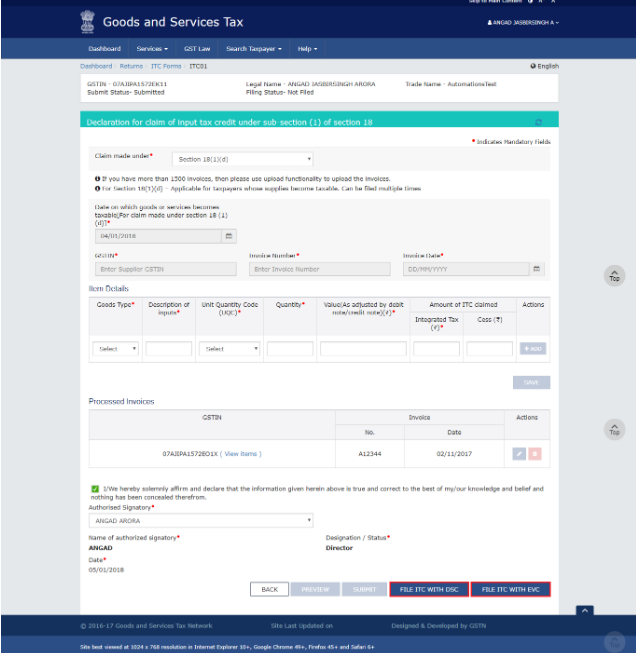

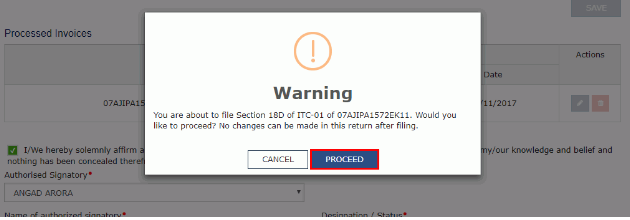

Final Submission

The data chosen by the taxpayer may freeze by clicking on the ‘Submit’ option, which effectively submits Form GST ITC-01. After submission, click the ‘Proceed’ option, which ultimately freezes the contents and makes it non-editable. The status of GST ITC-01 will reflect as submitted after the page is refreshed.

Submission

Submission

Proceed Option

Proceed Option

Status as Submitted

Status as Submitted

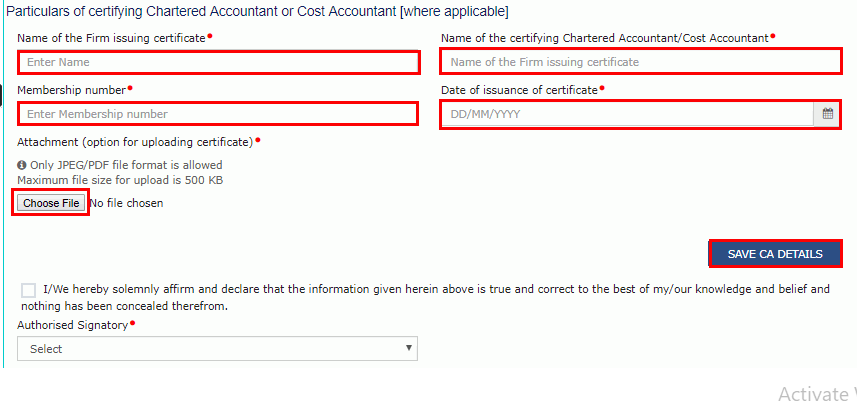

Updating Details of Certifying Chartered Accountants or Cost Accountant

If the value of an ITC range above Rs. 2 lakhs, the details of Chartered Accountant/Cost Accountant must be updated, in addition to the attachment of a CA/cost accountant certificate. For this purpose, the user needs to furnish the requisite details of the Chartered/Cost Accountant and save it on the portal. The details to be furnished include:

- Name of the firm issuing the certificate.

- Name of the certifying Chartered Accountant/Cost Accountant.

- Membership number of the Chartered or Cost Accountant.

- The date of issuance of the certificate.

Filing GST ITC-01 using DSC/EVC

The following steps will assist the user in the filing of GST ITC-01 using DSC/EVC:

Step 1: Checkbox Choose the checkbox. Step 2: Authorized Signatory Now, the authorized signatory may be chosen from the drop-down list, which enables the option of filing using DSC or EVC. Authorized Signatory

Authorized Signatory

Filing with DSC

Step 1: Select the Certificate Select the certificate by clicking on “Proceed.” Step 2: Sign Click on the option “Sign.” The Sign Option

The Sign Option

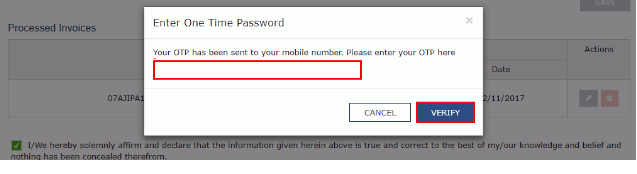

Filing with EVC

Step 1: OTP The authorized signatory will be sent an OTP in his/her registered number or e-mail, which must be entered to proceed to the final verification stage. Step 2: Verify Choose the option “Verify,” after which a success message will be displayed on the screen, along with the ARN. The status will now be displayed as filed. File with EVC

This effectively concludes the procedure of filing Form ITC GST-01.

File with EVC

This effectively concludes the procedure of filing Form ITC GST-01.

Input Tax Credit for Goods Received in Installments

If the recipient is receiving goods in instalments or parts, the claim of Input Tax Credit is only permissible after the receipt of the final lot of goods or instalment.

Input Tax Credit for Vehicles and Conveyance

To start with, the reader must understand that Input Tax Credit is generally not allowed to motor vehicles and conveyances, but for some exceptions. Here we focus on its exceptions i.e. on the facts where the applicant can avail Input Tax Credit for motor vehicles and conveyances.

Taxable supply of vehicles or conveyance

In this case where the taxpayer uses taxable supply for vehicle and conveyance, i.e. further supply of such vehicle or conveyance.

Supply of transportation of passengers

Input Tax Credit applies for transportation of passengers through motor vehicles or conveyances. This is not applicable if an assessee tries to transport his own employees free of cost, whereby he will be void of availing Input Tax Credit.

Imparting Training

If the taxpayer uses motor vehicles or conveyances into training with regards to driving, flying, navigating such vehicles or conveyances, the GST rules allow input tax credit.

Transportation of Goods

If vehicles and conveyances are used for transportation of Goods from one place to another, Input Tax Credit with respect to these vehicles and conveyances would be allowed.

Immovable Property

Scope of Input Tax Credit with regards to immovable property can be classified with two focal points:

- Input Tax Credit is not permissible for works contract services, supplied for immovable property, except in the case of plant and machinery, or input service for further supplies of work contract service.

- Goods or services received by a taxable person for construction of immovable property, except in the case of plant and machinery, including when the goods and services so supplied are used for the furtherance of business, are excluded from any claims under Input Tax Credit.

Goods or Services Not Eligible for Input Tax Credit

Availing Input Tax Credit by the taxpayer may become void for the following categories of goods and services:

- Supply of services such as outdoor catering, food and beverages, beauty treatment, health services, cosmetic surgery. The taxpayer however, would be eligible in cases of inward supply of goods or services used by a registered person for making an outward taxable supply, where the category of goods or supplied would be the same, or part of a taxable composite and mixed supply.

- Membership at a club, health and fitness centre.

- Cab Services, life or health insurance services.

- Travel benefits offered to employees during vocation or leave travel concession.

Gifts and Samples Not Eligible for Input Tax Credit.

Goods relinquished by way of gift or free samples, or through loss, robbery or destruction through any means, do not qualify for the claim in Input Tax Credit. Also, any person engaged in compensation in lieu of tax wouldn't be eligible to claim Input Tax Credit.

Time Limit for Claiming Input Tax Credit

An assessee will not be given the privilege to claim Input Tax Credit if he/she fails to claim the same while furnishing the returns due for the particular period. Also, any act of paying taxes through fraud, wilful misstatement, or suppression of facts would be held ineligible to the claim of Input Tax Credit.

Know more about Input Tax Credit in the guide below: https://www.indiafilings.com/learn/gst-input-tax-credit-guide/